As a real estate agent, you may be eligible to deduct expenses for the business use of your home. These expenses may include mortgage interest, insurance, utilities, repairs, and depreciation.

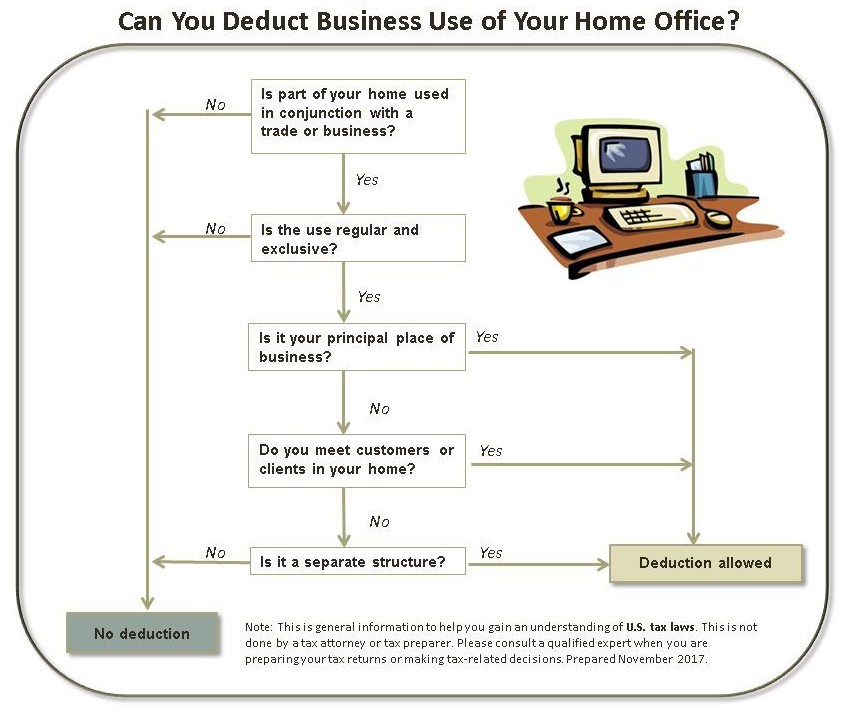

To qualify to claim expenses for the business use of your home, you must meet both of the following tests:

- The business part of your home must be used exclusively and regularly for your trade or business.

- The business part of your home must be:

- Your principal place of business; OR

- A place where you meet or deal with customers in the normal course of your business; OR

- A separate structure (not attached to your home) used in connection with your trade or business.

Here is a chart that can help illustrate if you qualify:

Other Guidelines

- You can use your home office for more than one business activity, but you cannot use it for any nonbusiness (that is, personal) activities.

- The area used for business can be a room or other separately identifiable space.

- The space does not need to be marked off by a permanent partition.

- You can deduct expenses for a separate free-standing structure, such as a studio, workshop, garage, or barn if you use it exclusively and regularly for your business. The structure does not have to be your principal place of business or a place where you meet clients or customers.

The following activities performed by you or others will not disqualify your home office from being your principal place of business.

- You have others conduct your administrative activities at locations other than your home. (For example, another company does your bookkeeping from its place of business.)

- You conduct administrative activities at places that are not fixed locations of your business, such as in a car or a hotel room.

- You occasionally conduct minimal administrative or management activities at a fixed location outside your home.

- You conduct substantial nonadministrative business activities at a fixed location outside your home. (For example, you meet with or provide services to customers or clients at a fixed location of the business outside your home.)

- You have suitable space to conduct administrative or management activities outside your home, but choose to use your home office for those activities instead.

** for more details, see IRS Publication 587 “Business Use of Your Home”

https://www.irs.gov/pub/irs-pdf/p587.pdf

Recent Comments